Everything you need to know about GST

Understanding GST can be difficult, especially given its frequent revisions, numerous compliance standards, and impact on businesses of all sizes. Whether you’re a startup owner, an experienced entrepreneur, or an individual attempting to understand taxation, having the appropriate knowledge is critical. In this blog, Team Taxperts, the best financial advisor in Kerala, explains all you need to know about Goods and Services Tax (GST), from the fundamentals and registration to filing, benefits, and common mistakes to avoid. With clear insights and practical advice, this guide will help you stay compliant and make better financial decisions. What is GST GST (Goods and Services Tax) is a unified indirect tax levied on the supply of goods and services in India. It replaced various indirect taxes such as VAT, service tax, excise duty, and others, bringing them under one common tax system. GST is intended to make taxation simpler, more transparent, and more efficient by removing the cascading impact of taxes. GST imposes tax at every stage of the supply chain, although firms can claim Input Tax Credit (ITC) for tax already paid on purchases. When Was GST Implemented in India GST was implemented in India on 1st July 2017. On this date, the Goods and Services Tax came into force, replacing several indirect taxes like as VAT, service tax, excise duty, and others, and establishing a unified tax system across the country under the notion of “One Nation, One Tax.” How Many Types of GST In India, there are four main types of GST: CGST (Central Goods and Services Tax): Collected by the Central Government on intra-state supplies of goods and services. SGST (State Goods and Services Tax): Collected by the State Government on intra-state supplies of goods and services. IGST (Integrated Goods and Services Tax): Collected by the Central Government on inter-state supplies and imports. UTGST (Union Territory Goods and Services Tax): Collected on intra-UT supplies in Union Territories without a legislature. When combined, these types guarantee efficient tax collection and revenue distribution among the Union Territories, States, and the Center. How GST Works GST operates on a value-added tax system, meaning that although taxes are levied at every point of the supply chain, the final consumer bears the majority of the tax burden. Here’s how it works simply: Tax at Every Stage: GST is levied whenever value is added—right from the manufacturer to the wholesaler, retailer, and finally the consumer. Input Tax Credit (ITC): Businesses can claim credit for the GST they have already paid on purchases. This means they pay tax only on the value they add, not on the entire transaction amount. Single Tax Structure: Instead of multiple indirect taxes, GST combines them into one system, reducing complexity and duplication. Intra-state and Inter-state Supply For sales within the same state, CGST and SGST are charged. For sales between different states, IGST is charged. Final Consumer Bears the Tax: While businesses collect and deposit GST with the government, the final cost of GST is borne by the end consumer. All things considered, GST guarantees transparency, prevents the cascading effect of taxes, and streamlines the tax system throughout India. What is GST Number A GST Number, also referred to as GSTIN (Goods and Services Tax Identification Number), is a distinctive 15-digit identification number provided to each organization or individual registered under GST in India. Structure of a GST Number First 2 digits: State code (as per Indian Census) Next 10 digits: PAN of the taxpayer 13th digit: Entity number (based on registrations under the same PAN) 14th digit: Default alphabet “Z” 15th digit: Check code (for error detection) Why a GST Number Is Important It allows businesses to collect and remit GST legally Mandatory for filing GST returns Required to claim Input Tax Credit (ITC) Helps in tracking transactions and ensuring compliance How to Apply for GST Number Obtaining a GST Number (GSTIN) in India is a simple online process. Here is an in-depth guide to help you comprehend how it operates: Check Eligibility: Before applying, ensure your business meets GST registration requirements based on turnover, type of business, or mandatory registration criteria. Visit the GST Portal: Go to the official GST portal and select the option for New Registration. Fill Part A of the Application Enter basic details such as: Legal name of the business PAN Email ID and mobile number An OTP will be sent for verification. Fill Part B of the Application After OTP verification, you will receive a Temporary Reference Number (TRN). Use this to complete the form by providing: Business address Nature of business activities Bank account details Details of promoters/partners/directors Upload required documents (PAN, address proof, photographs, bank proof) Submit Application with Digital Verification: Verify the application using DSC (Digital Signature Certificate), EVC, or Aadhaar authentication, and submit it. GSTIN Allotment: Once the application is verified and approved by the GST department, your GST Number (GSTIN) will be issued, usually within a few working days. GST registration is simple, but mistakes or missing information might cause delays or rejections. Consulting a skilled tax consultant in Kerala can assist in ensuring accurate filing, proper documentation, and seamless approval—especially for new and developing enterprises. How to Calculate GST Calculating GST is simple once you know the GST rate and whether the amount is exclusive or inclusive of GST. GST Calculation on an Amount (Exclusive of GST) Formula: GST Amount = (Original Price × GST Rate) ÷ 100 Total Price = Original Price + GST Amount Example: Original Price = ₹1,000 GST Rate = 18% GST = (1,000 × 18) ÷ 100 = ₹180 Total Price = ₹1,180 GST Calculation on an Amount (Inclusive of GST) Formula: GST Amount = [Original Price × GST Rate] ÷ (100 + GST Rate) Original Price = Total Price − GST Amount Example: Total Price (inclusive of GST) = ₹1,180 GST Rate = 18% GST = (1,180 × 18) ÷ 118 = ₹180 Original Price = ₹1,000 Common GST Rates in India 5%: Essential goods and services 12%: Standard goods

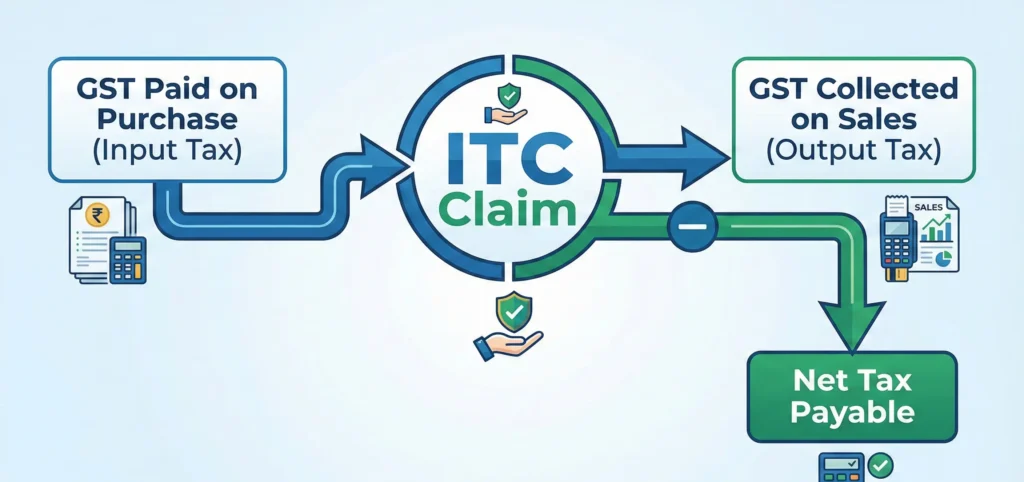

What is Input Tax Credit (ITC)

Input Tax Credit (ITC) is a GST system that allows firms to deduct the tax they have already paid on purchases from their overall output tax burden. In simpler terms, if your business buys goods or services and pays GST on them, you can claim that tax paid as a credit and offset it against the GST you need to pay on sales. This ensures that tax is only levied on the value contributed at each stage of the supply chain, preventing tax cascading. For accurate guidance on claiming ITC and maximizing tax benefits, Team Taxperts, a group of experienced tax professionals, can help. They are your go-to financial advisor in Kerala, providing knowledgeable guidance on ITC claims, GST, and general business financial planning. How Does ITC Work Input Tax Credit (ITC) enables businesses to lower the tax they pay on sales by using the GST they’ve already paid on purchases. The procedure is as follows, step-by-step: Purchase of Goods/Services: When a business buys goods or services, it pays GST to the supplier. Recording GST Paid: The GST paid on these purchases is recorded as input tax. Claiming ITC: When filing GST returns, the business can claim the GST paid on inputs as a credit. Offsetting Against Output Tax: The claimed ITC can be used to reduce the GST liability on sales (output tax). For example, if a business owes ₹10,000 in GST on sales but has ₹4,000 as ITC, it only needs to pay ₹6,000. Payment of Balance Tax: The remaining GST after applying ITC is paid to the government. Key Points: ITC can be claimed only if the goods/services are used for business purposes. Proper invoices and GST-compliant documentation are necessary to claim ITC. Why is Input Tax Credit Important Reduces Tax Burden: ITC allows businesses to offset the GST paid on purchases against the GST collected on sales, reducing the overall tax liability. Prevents Tax Cascading: Without ITC, tax would be charged on tax at every stage of production or supply. ITC ensures tax is levied only on the value added, preventing the “tax on tax” effect. Improves Cash Flow: By claiming ITC, businesses can lower the amount of GST they need to pay, helping maintain better cash flow for operations. Encourages Compliance: Businesses are motivated to maintain proper invoices and documentation to claim ITC, promoting transparency and accountability. Supports Business Growth: ITC helps reduce costs, making products and services more competitively priced, which can positively impact profitability and growth. Who All Are Eligible for Input Tax Credit Under GST, the following categories of taxpayers can claim ITC: Registered Businesses: Only GST-registered businesses can claim ITC. Unregistered entities are not eligible. Purchasers of Goods/Services for Business: ITC can be claimed on goods or services used for business purposes, such as raw materials, office supplies, or business-related services. Recipients of Taxable Supplies: Businesses receiving taxable goods or services (including imports) can claim ITC, provided GST has been paid by the supplier. Proper Documentation: Businesses must have a valid tax invoice, debit note, or other prescribed documents to claim ITC. Timely Filing: ITC can be claimed only if the GST returns are filed within the specified time under the GST laws. ITC is not available for personal use, motor vehicles (with a few exceptions), goods/services used for exempt supplies, or items like food and entertainment for personal consumption. How to Claim ITC Claiming ITC under GST involves a few key steps: = Ensure GST Registration: Only businesses registered under GST can claim ITC. Maintain Proper Documentation: Keep valid tax invoices, debit notes, or bills of supply for all purchases on which GST is paid. Check Eligibility: Ensure that the goods or services purchased are used for business purposes and are not excluded under GST rules. Match Supplier’s Details: Verify that the GST paid on purchases matches the details uploaded by the supplier in their GST returns. File GST Returns: Claim ITC while filing your monthly/quarterly GST returns (GSTR-3B). Enter the eligible credit in the designated ITC sections. Adjust Against Output Tax: Use the claimed ITC to offset your GST liability on sales. Pay only the balance tax, if any. Maintain Records: Keep all documents and records for at least 6 years, as they may be required during audits or assessments. How ITC Works in GST Input Tax Credit (ITC) under GST allows businesses to reduce their tax liability on sales by claiming credit for the GST already paid on purchases. Here’s how it works: Purchase of Goods/Services: A business buys goods or services and pays GST to the supplier. Recording GST Paid: The GST paid on these purchases is recorded as input tax. Claiming ITC: While filing GST returns, the business claims ITC on eligible purchases. Offsetting Against Output Tax: The ITC is used to reduce the GST payable on sales. Payment of Balance Tax: The remaining tax, after applying ITC, is paid to the government. Managing ITC and GST compliance can be difficult, especially with the regular changes in laws. Team Taxperts offers professional assistance for precise ITC computations and claims. Additionally, they provide accounting and bookkeeping services in India, assisting businesses in maintaining accurate, compliant, and structured financial records while maximising tax benefits. Benefits of Input Tax Credit Reduces Total Tax Liability: ITC allows businesses to use the GST paid on purchases to reduce the GST payable on sales, lowering their overall tax burden. Prevents Double Taxation: By eliminating the cascading effect (tax on tax), ITC ensures that tax is charged only on the value added at each stage. Improves Cash Flow: Since businesses pay only the net GST amount after applying ITC, it helps maintain better liquidity and smoother operations. Encourages Transparency: To claim ITC, businesses must maintain proper documentation and ensure supplier compliance, which promotes clean records and financial discipline. Enhances Profit Margins: Lower tax costs help reduce product or service pricing, improving profitability and market competitiveness. Supports Business Growth: With reduced financial strain and better cash management, businesses can reinvest in operations, expansion,

What is Udyam Registration?

Udyam Registration is a process established by the Government of India for the registration of Micro, Small, and Medium Enterprises (MSMEs) under the Ministry of Micro, Small, and Medium Enterprises. It is a component of the government’s initiatives to legalize companies and offer them subsidies, incentives, and programs intended to assist MSMEs. Purpose of Udyam Registration To officially recognize a business as an MSME. To make it easier for businesses to access government schemes, loans, and incentives. To simplify the process of applying for benefits and reduce paperwork. Who Can Register Any business operating in India, including proprietorships, partnerships, private limited companies, and LLPs. Both new and existing businesses can register. Udyam Registration Process Step 1: Prepare Required Documents Before starting the registration, make sure you have: Aadhaar number of the business owner (mandatory for proprietorships). PAN card of the business. Business details: Name, type (proprietorship, partnership, LLP, company), and address. Bank account details (optional but useful for linking). Details of investment in plant/equipment and annual turnover (to determine MSME category). Step 2: Visit the Official Portal Go to the official Udyam Registration website Step 3: Select the Registration Type For new businesses, click on “For New Entrepreneurs who are not Registered yet as MSME”. For existing businesses, use “For those having EM-II / UAM” (old registration number). Step 4: Fill in Business Details Enter Aadhaar number and name of the owner. The portal will verify Aadhaar via OTP sent to the registered mobile number. Fill in: Business name Type of organization (proprietorship, partnership, LLP, company) PAN card number Social category (optional) District and state Step 5: Enter Business Activities Specify whether your business is manufacturing or service. Describe your products or services. Step 6: Enter Investment and Turnover Details Investment in plant and machinery/equipment Annual turnover The portal will automatically classify your business as Micro, Small, or Medium based on these values. Step 7: Submit and Generate Udyam Registration Number Review the details carefully. Apply. The portal will generate a Udyam Registration Number (URN) instantly. You will also get a registration certificate in PDF format. Step 8: Keep the Certificate Safe The Udyam Registration Certificate serves as proof of being an MSME. It can be used for: Bank loans at concessional rates Government subsidies and incentives Bidding for government tenders Documents Needed for Udyam Registration For Udyam Registration, the process is supposed to be quick and mostly online; therefore, any documents required are minimal. Here is a concise list: Aadhaar Number Mandatory for the business owner (for proprietorships). Used for identity verification via OTP. For other business types (partnership, LLP, company), Aadhaar of the authorized signatory is required. PAN Card PAN of the business or the business owner is required. Helps in linking the business for tax purposes. Business Details Business name Type of organization: Proprietorship, Partnership, LLP, Private Limited, Public Limited, etc. Address of business (physical address is mandatory) Bank Account Details (Optional but Recommended) Bank account number IFSC code Helps with subsidies, schemes, and government payments Investment & Turnover Details Investment in plant and machinery/equipment (for manufacturing or service activities) Annual turnover (for MSME classification: Micro, Small, Medium) Additional (Optional) Social category: SC/ST/OBC if applicable Details of business activities: Manufacturing or Service, products, or services offered How to Get Udyam Registration Number Step 1: Visit the Official Portal Go to the official government website: This is the only authentic site for MSME registration. Step 2: Choose “For New Entrepreneurs” Click on the option: “For New Entrepreneurs who are not registered yet as MSMEs.” If you already have UAM or EM-II, choose the second option. Step 3: Enter Aadhaar Number Provide the Aadhaar number of the business owner (proprietor) or authorized signatory. Verify Aadhaar using the OTP sent to the registered mobile number. Step 4: Enter PAN Details Enter PAN of the business (for companies, LLPs, partnership firms) or PAN of the owner (for proprietorships). The portal automatically validates PAN from the government database. Step 5: Fill Business Information You must provide: Business name Type of enterprise (proprietorship, partnership, LLP, Pvt Ltd, etc.) Full business address Bank details (optional but recommended) Major business activity (manufacturing or service) Step 6: Add Investment & Turnover Details Enter details like: Investment in machinery/equipment Annual turnover These details help classify your business as Micro, Small, or Medium. Step 7: Submit the Application Review all details. Click Submit. Validate using OTP Step 8: Receive Udyam Registration Number (URN) Once submitted: You instantly receive the Udyam Registration Number (URN) on the screen. The same will also be sent to your registered email address. Step 9: Download Udyam Registration Certificate After getting the URN: You can download your official Udyam Registration Certificate (PDF) from the portal. Udyam Registration Benefits Easy Access to Loans & Credit MSMEs get priority in bank loans. Eligibility for collateral-free loans under schemes like CGTMSE. Lower interest rates compared to regular business loans. Government Subsidies Businesses with Udyam Registration can get: Subsidy on patent registration Subsidy on ISO certification Subsidy on electricity bills Financial support for technology upgradation Priority in Government Tenders MSMEs get preference in public procurement. Many tenders are reserved exclusively for MSMEs. EMD (Earnest Money Deposit) and security deposit waivers in many cases. Protection Against Delayed Payments If buyers delay payment beyond 45 days, the MSME can: File a complaint on the MSME Samadhaan Portal Claim interest on delayed payments Helps small businesses maintain healthy cash flow. Easier to Participate in Government Schemes Eligible for various MSME-focused schemes: PMEGP (Prime Minister Employment Generation Programme) Cluster development programs Technology and Quality Upgradation Programs Zero Defect Zero Effect scheme Financial & Tax Benefits Lower cost of bank processing fees Concession on stamp duty & registration fees for business setup in some states Special credit-linked incentives Enhances Business Credibility Shows your business is officially recognized by the Government of India. Increases trust among banks, customers, and vendors. Eligibility for International & Domestic Trade Fairs MSMEs can participate in trade fairs with subsidized fees. Support for export promotion and global

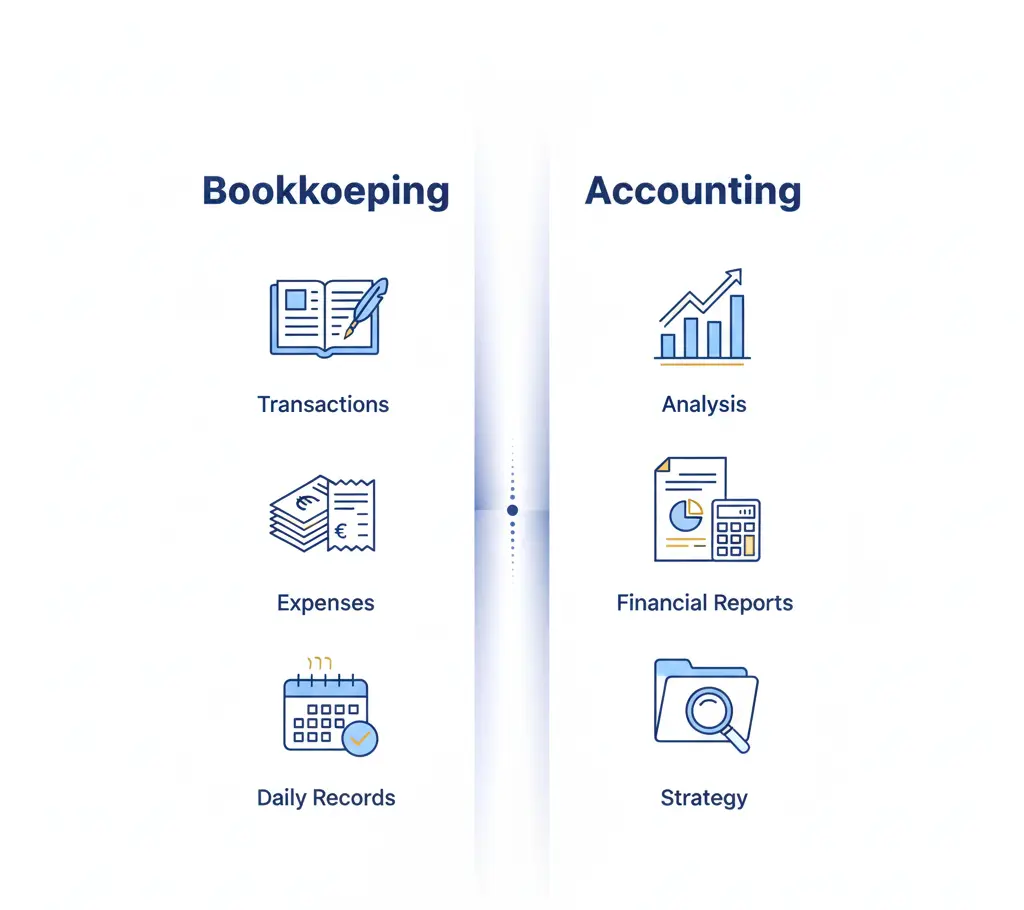

What is the Difference Between Bookkeeping and Accounting

Understanding your company’s finances begins with two fundamental pillars: bookkeeping and accounting. Although these terms are frequently used interchangeably, they serve quite different purposes in keeping a corporation financially healthy. While accounting reads, analyzes, and turns that data into insightful information, bookkeeping concentrates on accurately recording daily transactions. In this blog, we’ll look at the major distinctions between bookkeeping and accounting, why they’re important, and how they operate together to enable wise decision-making and long-term growth. Whether you’re a small business owner or just entering into the world of finance, this guide will give you a clear and simple understanding of the two. At Team Taxperts, we simplify these processes for businesses by providing dependable accounting and bookkeeping services in India, assuring accuracy, compliance, and clarity at every stage. What is Bookkeeping Bookkeeping is the process of recording, organizing, and upholding all the financial transactions of a business daily. It entails tracking every sale, purchase, payment, invoice, and expense to verify that the company’s financial records are correct and up to date. Bookkeeping typically includes tasks like: Recording transactions in ledgers or software Managing invoices and receipts Tracking expenses and payments Reconciling bank statements Maintaining financial documents What is Accounting? Accounting is the process of interpreting, analyzing, and summarizing a company’s financial data to help make better decisions. While bookkeeping is concerned with recording financial data, accounting transforms that information into relevant reports. Accounting typically includes tasks such as: Preparing financial statements (like balance sheets, income statements, and cash flow statements) Analyzing profits, losses, and financial trends Budgeting and forecasting Ensuring tax compliance Helping with strategic planning and business growth Difference Between Bookkeeping and Accounting Although bookkeeping and accounting are closely related, they perform distinct functions in managing a company’s finances. Purpose Bookkeeping: Focuses on recording daily financial transactions. Accounting: Focuses on interpreting and analyzing those recorded transactions. Scope of Work Bookkeeping: Involves tasks like maintaining ledgers, tracking expenses, issuing invoices, and reconciling accounts. Accounting: Includes preparing financial statements, budgeting, tax planning, auditing, and offering financial insights. Objective Bookkeeping: Ensures accurate and organized financial data. Accounting: Uses that data to assess financial health and guide business decisions. Skills Required Bookkeeping: More transactional and administrative — requires attention to detail. Accounting: Requires analytical thinking, financial expertise, and knowledge of tax laws and reporting standards. Output Bookkeeping: Produces raw financial records. Accounting: Produces meaningful reports, insights, and strategies. Final Thoughts Bookkeeping and accounting may serve distinct tasks, yet together they constitute the foundation of any company’s financial health. While bookkeeping guarantees reliable, structured records, accounting turns those records into helpful insights that guide smarter decisions, strategic planning, and profitable development. Having the proper experts on your side is crucial for companies trying to maintain compliance and simplify their finances. That is why many businesses prefer to hire financial advisor India professionals that can manage both bookkeeping and accounting tasks with knowledge and precision. With the correct assistance, managing your financial health becomes easier, more obvious, and strategic. Reach out to Taxperts to streamline your bookkeeping and accounting needs.