What is Input Tax Credit (ITC)

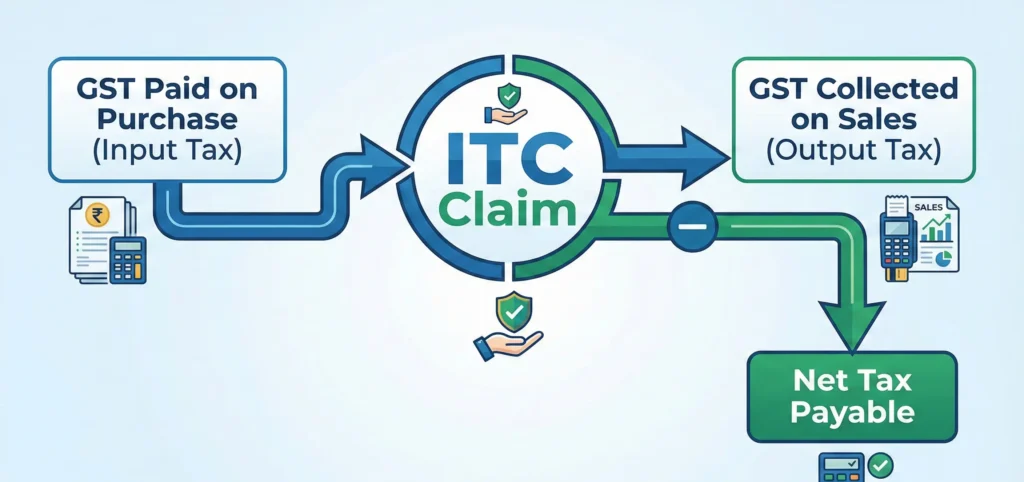

Input Tax Credit (ITC) is a GST system that allows firms to deduct the tax they have already paid on purchases from their overall output tax burden. In simpler terms, if your business buys goods or services and pays GST on them, you can claim that tax paid as a credit and offset it against the GST you need to pay on sales. This ensures that tax is only levied on the value contributed at each stage of the supply chain, preventing tax cascading. For accurate guidance on claiming ITC and maximizing tax benefits, Team Taxperts, a group of experienced tax professionals, can help. They are your go-to financial advisor in Kerala, providing knowledgeable guidance on ITC claims, GST, and general business financial planning. How Does ITC Work Input Tax Credit (ITC) enables businesses to lower the tax they pay on sales by using the GST they’ve already paid on purchases. The procedure is as follows, step-by-step: Purchase of Goods/Services: When a business buys goods or services, it pays GST to the supplier. Recording GST Paid: The GST paid on these purchases is recorded as input tax. Claiming ITC: When filing GST returns, the business can claim the GST paid on inputs as a credit. Offsetting Against Output Tax: The claimed ITC can be used to reduce the GST liability on sales (output tax). For example, if a business owes ₹10,000 in GST on sales but has ₹4,000 as ITC, it only needs to pay ₹6,000. Payment of Balance Tax: The remaining GST after applying ITC is paid to the government. Key Points: ITC can be claimed only if the goods/services are used for business purposes. Proper invoices and GST-compliant documentation are necessary to claim ITC. Why is Input Tax Credit Important Reduces Tax Burden: ITC allows businesses to offset the GST paid on purchases against the GST collected on sales, reducing the overall tax liability. Prevents Tax Cascading: Without ITC, tax would be charged on tax at every stage of production or supply. ITC ensures tax is levied only on the value added, preventing the “tax on tax” effect. Improves Cash Flow: By claiming ITC, businesses can lower the amount of GST they need to pay, helping maintain better cash flow for operations. Encourages Compliance: Businesses are motivated to maintain proper invoices and documentation to claim ITC, promoting transparency and accountability. Supports Business Growth: ITC helps reduce costs, making products and services more competitively priced, which can positively impact profitability and growth. Who All Are Eligible for Input Tax Credit Under GST, the following categories of taxpayers can claim ITC: Registered Businesses: Only GST-registered businesses can claim ITC. Unregistered entities are not eligible. Purchasers of Goods/Services for Business: ITC can be claimed on goods or services used for business purposes, such as raw materials, office supplies, or business-related services. Recipients of Taxable Supplies: Businesses receiving taxable goods or services (including imports) can claim ITC, provided GST has been paid by the supplier. Proper Documentation: Businesses must have a valid tax invoice, debit note, or other prescribed documents to claim ITC. Timely Filing: ITC can be claimed only if the GST returns are filed within the specified time under the GST laws. ITC is not available for personal use, motor vehicles (with a few exceptions), goods/services used for exempt supplies, or items like food and entertainment for personal consumption. How to Claim ITC Claiming ITC under GST involves a few key steps: = Ensure GST Registration: Only businesses registered under GST can claim ITC. Maintain Proper Documentation: Keep valid tax invoices, debit notes, or bills of supply for all purchases on which GST is paid. Check Eligibility: Ensure that the goods or services purchased are used for business purposes and are not excluded under GST rules. Match Supplier’s Details: Verify that the GST paid on purchases matches the details uploaded by the supplier in their GST returns. File GST Returns: Claim ITC while filing your monthly/quarterly GST returns (GSTR-3B). Enter the eligible credit in the designated ITC sections. Adjust Against Output Tax: Use the claimed ITC to offset your GST liability on sales. Pay only the balance tax, if any. Maintain Records: Keep all documents and records for at least 6 years, as they may be required during audits or assessments. How ITC Works in GST Input Tax Credit (ITC) under GST allows businesses to reduce their tax liability on sales by claiming credit for the GST already paid on purchases. Here’s how it works: Purchase of Goods/Services: A business buys goods or services and pays GST to the supplier. Recording GST Paid: The GST paid on these purchases is recorded as input tax. Claiming ITC: While filing GST returns, the business claims ITC on eligible purchases. Offsetting Against Output Tax: The ITC is used to reduce the GST payable on sales. Payment of Balance Tax: The remaining tax, after applying ITC, is paid to the government. Managing ITC and GST compliance can be difficult, especially with the regular changes in laws. Team Taxperts offers professional assistance for precise ITC computations and claims. Additionally, they provide accounting and bookkeeping services in India, assisting businesses in maintaining accurate, compliant, and structured financial records while maximising tax benefits. Benefits of Input Tax Credit Reduces Total Tax Liability: ITC allows businesses to use the GST paid on purchases to reduce the GST payable on sales, lowering their overall tax burden. Prevents Double Taxation: By eliminating the cascading effect (tax on tax), ITC ensures that tax is charged only on the value added at each stage. Improves Cash Flow: Since businesses pay only the net GST amount after applying ITC, it helps maintain better liquidity and smoother operations. Encourages Transparency: To claim ITC, businesses must maintain proper documentation and ensure supplier compliance, which promotes clean records and financial discipline. Enhances Profit Margins: Lower tax costs help reduce product or service pricing, improving profitability and market competitiveness. Supports Business Growth: With reduced financial strain and better cash management, businesses can reinvest in operations, expansion,

What is Udyam Registration?

Udyam Registration is a process established by the Government of India for the registration of Micro, Small, and Medium Enterprises (MSMEs) under the Ministry of Micro, Small, and Medium Enterprises. It is a component of the government’s initiatives to legalize companies and offer them subsidies, incentives, and programs intended to assist MSMEs. Purpose of Udyam Registration To officially recognize a business as an MSME. To make it easier for businesses to access government schemes, loans, and incentives. To simplify the process of applying for benefits and reduce paperwork. Who Can Register Any business operating in India, including proprietorships, partnerships, private limited companies, and LLPs. Both new and existing businesses can register. Udyam Registration Process Step 1: Prepare Required Documents Before starting the registration, make sure you have: Aadhaar number of the business owner (mandatory for proprietorships). PAN card of the business. Business details: Name, type (proprietorship, partnership, LLP, company), and address. Bank account details (optional but useful for linking). Details of investment in plant/equipment and annual turnover (to determine MSME category). Step 2: Visit the Official Portal Go to the official Udyam Registration website Step 3: Select the Registration Type For new businesses, click on “For New Entrepreneurs who are not Registered yet as MSME”. For existing businesses, use “For those having EM-II / UAM” (old registration number). Step 4: Fill in Business Details Enter Aadhaar number and name of the owner. The portal will verify Aadhaar via OTP sent to the registered mobile number. Fill in: Business name Type of organization (proprietorship, partnership, LLP, company) PAN card number Social category (optional) District and state Step 5: Enter Business Activities Specify whether your business is manufacturing or service. Describe your products or services. Step 6: Enter Investment and Turnover Details Investment in plant and machinery/equipment Annual turnover The portal will automatically classify your business as Micro, Small, or Medium based on these values. Step 7: Submit and Generate Udyam Registration Number Review the details carefully. Apply. The portal will generate a Udyam Registration Number (URN) instantly. You will also get a registration certificate in PDF format. Step 8: Keep the Certificate Safe The Udyam Registration Certificate serves as proof of being an MSME. It can be used for: Bank loans at concessional rates Government subsidies and incentives Bidding for government tenders Documents Needed for Udyam Registration For Udyam Registration, the process is supposed to be quick and mostly online; therefore, any documents required are minimal. Here is a concise list: Aadhaar Number Mandatory for the business owner (for proprietorships). Used for identity verification via OTP. For other business types (partnership, LLP, company), Aadhaar of the authorized signatory is required. PAN Card PAN of the business or the business owner is required. Helps in linking the business for tax purposes. Business Details Business name Type of organization: Proprietorship, Partnership, LLP, Private Limited, Public Limited, etc. Address of business (physical address is mandatory) Bank Account Details (Optional but Recommended) Bank account number IFSC code Helps with subsidies, schemes, and government payments Investment & Turnover Details Investment in plant and machinery/equipment (for manufacturing or service activities) Annual turnover (for MSME classification: Micro, Small, Medium) Additional (Optional) Social category: SC/ST/OBC if applicable Details of business activities: Manufacturing or Service, products, or services offered How to Get Udyam Registration Number Step 1: Visit the Official Portal Go to the official government website: This is the only authentic site for MSME registration. Step 2: Choose “For New Entrepreneurs” Click on the option: “For New Entrepreneurs who are not registered yet as MSMEs.” If you already have UAM or EM-II, choose the second option. Step 3: Enter Aadhaar Number Provide the Aadhaar number of the business owner (proprietor) or authorized signatory. Verify Aadhaar using the OTP sent to the registered mobile number. Step 4: Enter PAN Details Enter PAN of the business (for companies, LLPs, partnership firms) or PAN of the owner (for proprietorships). The portal automatically validates PAN from the government database. Step 5: Fill Business Information You must provide: Business name Type of enterprise (proprietorship, partnership, LLP, Pvt Ltd, etc.) Full business address Bank details (optional but recommended) Major business activity (manufacturing or service) Step 6: Add Investment & Turnover Details Enter details like: Investment in machinery/equipment Annual turnover These details help classify your business as Micro, Small, or Medium. Step 7: Submit the Application Review all details. Click Submit. Validate using OTP Step 8: Receive Udyam Registration Number (URN) Once submitted: You instantly receive the Udyam Registration Number (URN) on the screen. The same will also be sent to your registered email address. Step 9: Download Udyam Registration Certificate After getting the URN: You can download your official Udyam Registration Certificate (PDF) from the portal. Udyam Registration Benefits Easy Access to Loans & Credit MSMEs get priority in bank loans. Eligibility for collateral-free loans under schemes like CGTMSE. Lower interest rates compared to regular business loans. Government Subsidies Businesses with Udyam Registration can get: Subsidy on patent registration Subsidy on ISO certification Subsidy on electricity bills Financial support for technology upgradation Priority in Government Tenders MSMEs get preference in public procurement. Many tenders are reserved exclusively for MSMEs. EMD (Earnest Money Deposit) and security deposit waivers in many cases. Protection Against Delayed Payments If buyers delay payment beyond 45 days, the MSME can: File a complaint on the MSME Samadhaan Portal Claim interest on delayed payments Helps small businesses maintain healthy cash flow. Easier to Participate in Government Schemes Eligible for various MSME-focused schemes: PMEGP (Prime Minister Employment Generation Programme) Cluster development programs Technology and Quality Upgradation Programs Zero Defect Zero Effect scheme Financial & Tax Benefits Lower cost of bank processing fees Concession on stamp duty & registration fees for business setup in some states Special credit-linked incentives Enhances Business Credibility Shows your business is officially recognized by the Government of India. Increases trust among banks, customers, and vendors. Eligibility for International & Domestic Trade Fairs MSMEs can participate in trade fairs with subsidized fees. Support for export promotion and global market

What is the Difference Between Bookkeeping and Accounting

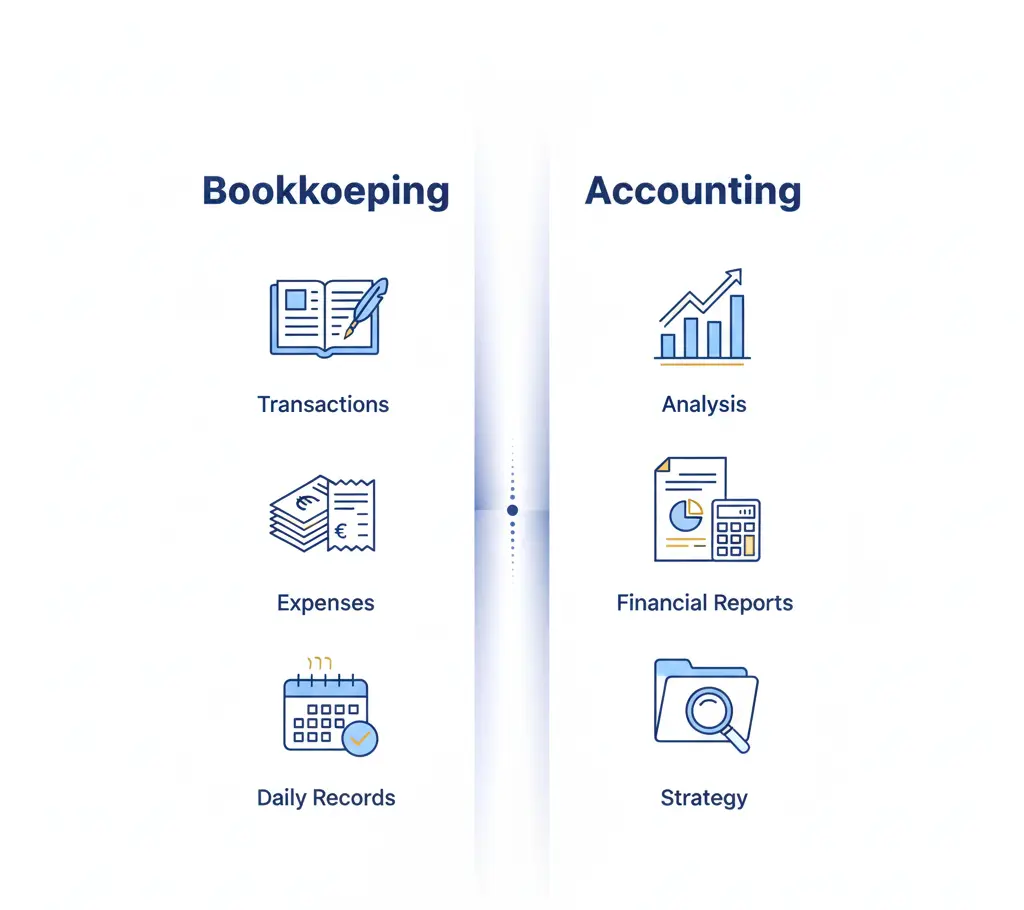

Understanding your company’s finances begins with two fundamental pillars: bookkeeping and accounting. Although these terms are frequently used interchangeably, they serve quite different purposes in keeping a corporation financially healthy. While accounting reads, analyzes, and turns that data into insightful information, bookkeeping concentrates on accurately recording daily transactions. In this blog, we’ll look at the major distinctions between bookkeeping and accounting, why they’re important, and how they operate together to enable wise decision-making and long-term growth. Whether you’re a small business owner or just entering into the world of finance, this guide will give you a clear and simple understanding of the two. At Team Taxperts, we simplify these processes for businesses by providing dependable accounting and bookkeeping services in India, assuring accuracy, compliance, and clarity at every stage. What is Bookkeeping Bookkeeping is the process of recording, organizing, and upholding all the financial transactions of a business daily. It entails tracking every sale, purchase, payment, invoice, and expense to verify that the company’s financial records are correct and up to date. Bookkeeping typically includes tasks like: Recording transactions in ledgers or software Managing invoices and receipts Tracking expenses and payments Reconciling bank statements Maintaining financial documents What is Accounting? Accounting is the process of interpreting, analyzing, and summarizing a company’s financial data to help make better decisions. While bookkeeping is concerned with recording financial data, accounting transforms that information into relevant reports. Accounting typically includes tasks such as: Preparing financial statements (like balance sheets, income statements, and cash flow statements) Analyzing profits, losses, and financial trends Budgeting and forecasting Ensuring tax compliance Helping with strategic planning and business growth Difference Between Bookkeeping and Accounting Although bookkeeping and accounting are closely related, they perform distinct functions in managing a company’s finances. Purpose Bookkeeping: Focuses on recording daily financial transactions. Accounting: Focuses on interpreting and analyzing those recorded transactions. Scope of Work Bookkeeping: Involves tasks like maintaining ledgers, tracking expenses, issuing invoices, and reconciling accounts. Accounting: Includes preparing financial statements, budgeting, tax planning, auditing, and offering financial insights. Objective Bookkeeping: Ensures accurate and organized financial data. Accounting: Uses that data to assess financial health and guide business decisions. Skills Required Bookkeeping: More transactional and administrative — requires attention to detail. Accounting: Requires analytical thinking, financial expertise, and knowledge of tax laws and reporting standards. Output Bookkeeping: Produces raw financial records. Accounting: Produces meaningful reports, insights, and strategies. Final Thoughts Bookkeeping and accounting may serve distinct tasks, yet together they constitute the foundation of any company’s financial health. While bookkeeping guarantees reliable, structured records, accounting turns those records into helpful insights that guide smarter decisions, strategic planning, and profitable development. Having the proper experts on your side is crucial for companies trying to maintain compliance and simplify their finances. That is why many businesses prefer to hire financial advisor India professionals that can manage both bookkeeping and accounting tasks with knowledge and precision. With the correct assistance, managing your financial health becomes easier, more obvious, and strategic. Reach out to Taxperts to streamline your bookkeeping and accounting needs.

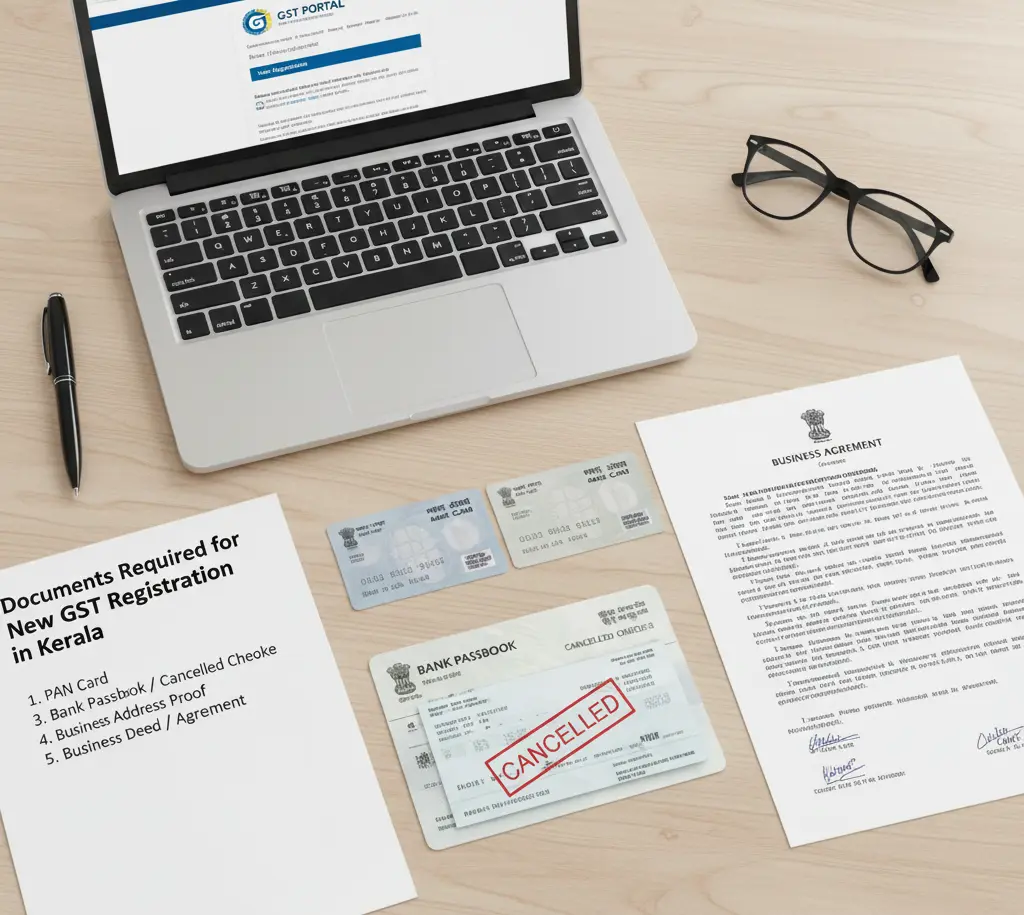

Documents Required for New GST Registration in Kerala

Starting a new business in Kerala? One of the first and most critical procedures is to complete your GST registration properly. Whether you’re a new entrepreneur, a small business owner, or expanding an existing venture, GST registration is required whenever you reach the prescribed revenue threshold. However, before you start the online process, having the necessary paperwork ready can save you time, prevent rejections, and ensure an effortless approval. In this blog, we’ll cover the primary documents required for new GST registration in Kerala, explain their importance, and guide how to upload them correctly. Let’s get you GST-ready the effortless way. These are the Documents Required for New GST Registration in Kerala To ensure a seamless and effective GST registration procedure in Kerala, businesses must provide appropriate documents verifying their name, business location, and financial information. Every document is essential to proving the applicant’s legitimacy and avoiding inconsistencies during verification. Here’s a detailed explanation of what you require and why: PAN: The Permanent Account Number (PAN) is a mandatory identifying document for GST registration. For individuals, the personal PAN is required, while for businesses such as partnerships, companies, or LLPs, the PAN of the organization must be submitted. It serves as the key tax identifier and connects all financial transactions into a single system. Identity and Address Proof with Photograph: Candidates must provide proof of identification and address, such as a driver’s license, passport, voter ID, or Aadhaar. These documents authenticate the applicant’s legitimacy and ensure that the GST registration is granted to a verified individual. A clean, current photograph is also necessary for supplementary identity verification. Proof of Business Address: To prove the physical address of your company, you must supply paperwork such as a rental agreement, utility bill, property tax receipt, or ownership document. This aids GST authorities in making sure that business operations are carried out at a legitimate and traceable address. Bank Account Details: Bank account information is required for integrating your business transactions into the GST system. A cancelled cheque, a copy of your passbook, or a bank statement can be submitted. These records aid in verifying the financial account linked to your company for compliance, payments, and refunds. Authorization Letter / Board Resolution: If your GST application is being filed by an authorized signatory rather than the business owner, you must provide a permission letter or board resolution. This document certifies that the person managing the GST processes is authorized to act on the company’s or entity’s behalf. Additional Documents Based on Business Structure Apart from the basic documents required for GST registration, Kerala businesses must also provide documentation unique to their business structure. These extra records assist authorities in confirming the entity’s ownership, legal establishment, and operational authorization. Sole Proprietorship: Sole proprietors must produce documents establishing their identity and ownership of the business. Typical supplementary documents consist of: Owner’s Aadhaar Card Owner’s PAN (mandatory as business PAN is not applicable) Trade license / Shop & Establishment Certificate These documents guarantee the legal recognition of the business and its owner as the same. Partnership Firm Documents attesting to the partnership’s existence and partners’ rights must be provided by partnership firms. Among them are: Partnership Deed PAN of the Partnership Firm Authorization letter from the partners Partner’s ID and address proof These documents affirm the legal structure and specify which partners are responsible for GST compliance. Limited Liability Partnership (LLP) Since LLPs are incorporated entities, their establishment must be validated by extralegal documents. These include: LLP Agreement Certificate of Incorporation issued by the Ministry of Corporate Affairs (MCA) Resolution appointing an authorized signatory Designated partners’ ID and address proof This guarantees that the firm complies with MCA standards and GST requirements. Private Limited Company Private limited corporations are required to submit thorough documentation proving their corporate identity and authorized representation. These include: Certificate of Incorporation issued by MCA Memorandum and Articles of Association (MOA & AOA) Board Resolution authorizing a director for GST activities Director’s ID and address proofs (DIN, PAN, Aadhaar, etc.) These records attest to the organization’s legal standing, governing body, and authorized staff. Final Thoughts The first step towards a fast and hassle-free GST registration in Kerala is to ensure that you have the necessary paperwork. From fundamental identity proofs to business structure-specific documentation, each criterion is critical to authenticating your firm and avoiding approval delays. Whether you’re a new entrepreneur or expanding your business, maintaining compliance from the start helps you develop a solid financial foundation. If you require expert guidance throughout the process, Taxperts can help you with professional support, precise documentation, and end-to-end compliance. For a smooth experience, always hire the best financial advisor in India—someone who genuinely understands the state’s regulatory system and ensures everything is done correctly. Are you prepared to have a stress-free GST journey? Let Taxperts take care of the details so you can concentrate on expanding your company.

Retirement Planning Tips for NRI

Introduction – NRI Retirement Planning for retirement is an essential step for everyone, but for Keralites, particularly for NRIs who are thinking of coming back home after years abroad, it possesses an even greater significance. The shift from an active profession abroad to a calm existence in India necessitates more than just savings; it also necessitates clarity, structure, and timely financial decisions. Proper tax planning and a well-thought-out investment strategy are critical in guaranteeing financial stability, protecting your money, and allowing you to live a stress-free post-retirement life. For NRIs, retirement planning entails understanding cross-border tax restrictions, selecting the best investment opportunities in India, obtaining healthcare, and establishing a corpus large enough to withstand inflation and lifestyle expenses. With the correct retirement planning tips for NRIs, you may make your return to Kerala easier, more financially secure, and really rewarding. Why NRIs and Kerala Residents Need Retirement Planning Retirement planning is vital for everyone, but NRIs and Kerala residents have distinct financial concerns. Many NRIs make money in foreign currencies that fluctuate, and their earnings frequently change based on the state of the world economy. This makes long-term financial stability more difficult to forecast unless accompanied by a robust, well-planned savings and investment strategy. A comfortable salary earned overseas might not be worth the same amount when translated into Indian rupees years later due to currency exchange rates. Family responsibilities offer a new level of difficulty. Keralites have traditionally supported old parents, educated children, and, on occasion, provided for extended family members, emphasizing the need of having a good financial strategy. Long-term settlement decisions for NRIs returning to Kerala, such as purchasing property, obtaining health insurance, or establishing a retirement fund, necessitate careful consideration and early planning. Furthermore, the rising cost of living and continually rising medical costs in Kerala make it even more necessary to plan. Healthcare, in particular, can become a considerable cost during retirement if not properly planned for. With appropriate planning, NRIs and Kerala natives can ensure their financial future, maintain their lifestyle, and retire in peace and security in their homeland. Factors to Consider Before Planning Retirement Before creating your retirement plan, consider a few critical elements that can impact your long-term financial security: Where You Plan to Settle (India or Abroad): Your retirement location influences your living expenditures, healthcare requirements, tax laws, and even the types of investments that will work best for you. Whether you choose to stay abroad or settle back in India, particularly in Kerala, your financial approach ought to comply with your future living environment. Expected Expenses After Retirement: Estimate your post-retirement expenses, such as housing, food, healthcare, travel, and leisure. Living costs in Kerala are rising gradually, especially for medical care, making accurate expense estimation essential for long-term comfort. Tax Implications of Foreign and Indian Income: NRIs must evaluate how their income, whether earned overseas, repatriated, or created through investments in India, will be taxed. Understanding double taxation rules, NRE/NRO account taxation, and residency status can help maximize returns and prevent excessive tax burdens. Investment Liquidity and Safety: A strong retirement portfolio strikes the right balance between growth and safety. Give top priority to assets that provide steady returns and simple liquidity in times of need. NRIs should also carefully assess risk levels to ensure that their retirement funds are protected against market fluctuations. Best Retirement Investment Options for NRIs Planning for a solid financial future is made easier when you select the correct balance of steady and growth-oriented assets. Here are some of the most trusted retirement investment alternatives for NRIs: NPS (National Pension System): NPS is a good long-term retirement option for NRIs with Indian bank accounts. It provides professional fund management, market-linked returns, and tax advantages. A portion can be taken out in one lump amount at retirement, while the remainder offers lifetime pension income. EPF (Employees’ Provident Fund) for Returning NRIs: NRIs who have previously worked in India and made contributions to the Employee Provident Fund (EPF) may continue to get benefits if they return. EPF serves as a reliable retirement safety net and offers secure, fixed-interest returns, particularly for individuals returning to the Indian job market. PPF (Public Provident Fund): PPF is a government-backed investment with a 15-year lock-in that offers long-term, tax-free earnings. Though NRIs are not permitted to register new PPF accounts, existing ones (opened prior to NRI status) can be maintained till maturity, making it a safe option for retirement savings. NRE/NRO Fixed Deposits: These fixed deposits are preferred among NRIs due to their stability. NRE FDs: Tax-free in India, fully repatriable, but interest rates may be lower. NRO FDs: Higher interest rates but taxable in India; useful for income earned within the country. Both options provide guaranteed returns and low risk. Mutual Funds / SIPs: Mutual funds and SIPs provide flexibility and long-term wealth growth for NRIs looking for greater returns. Equity, debt, and hybrid funds can be selected based on risk tolerance. Many AMCs allow NRIs to invest with the correct KYC and documents. Real Estate in Kerala: Purchasing property in Kerala provides two purposes: an appreciating investment and a future retirement home. Whether you’re building a house, buying a villa, or investing in a rental property, real estate can help you achieve both financial and lifestyle goals for your return. Tax Planning for NRI Retirement Tax planning is an essential aspect of NRI retirement planning, particularly for those wanting to return to India. Understanding how taxes apply to various sources of income ensures that your savings are protected and your post-retirement cash flow is consistent. How Indian Taxation Applies to NRIs Non-resident Indians are taxed exclusively on income generated or received within India. This comprises: Investment income: Returns from NRE/NRO fixed deposits, mutual funds, and other financial instruments. Pension income: Pensions received in India are taxable depending on the individual’s income slab. Rental income from property: Rent received from property in Kerala or elsewhere in India is taxable, though certain deductions (like a standard 30% deduction, municipal